- Industries

Industries

- Functions

Functions

- Insights

Insights

- Careers

Careers

- About Us

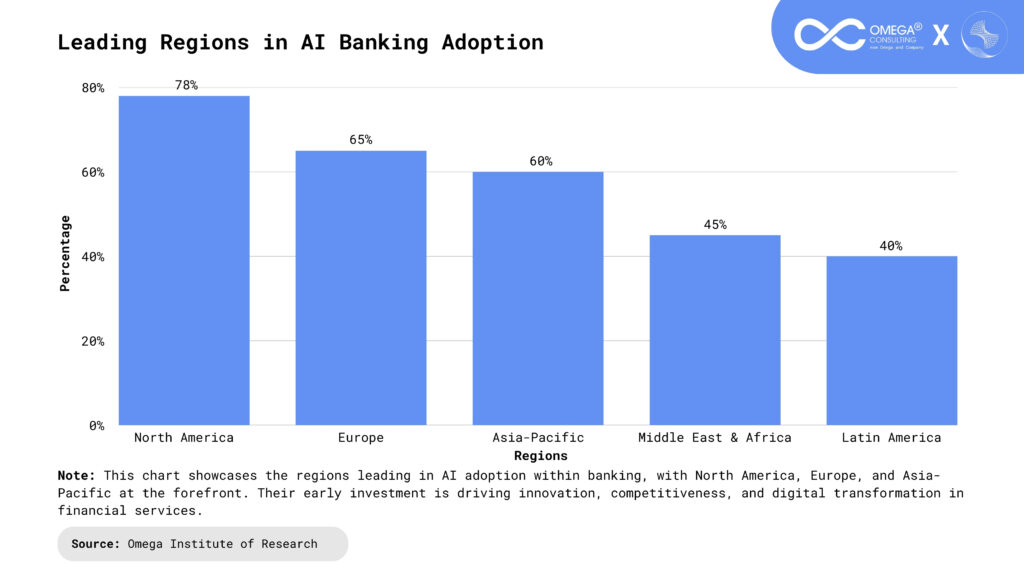

AI in Banking

Artificial Intelligence (AI) is no longer just a buzzword, it’s a driving force behind the transformation of banking as we know it. From chatbots to algorithmic credit assessments, AI is helping financial institutions become more agile, efficient, and customer-focused. As the demand for digital-first experiences grows, banks are tapping into AI to stay competitive and future-ready. AI-powered fraud detection systems now analyze vast datasets in real time to flag suspicious activities, enhancing security across banking operations. Personalized financial insights delivered through AI are empowering customers to make smarter money decisions. Moreover, AI is streamlining compliance and regulatory processes, reducing risk and operational burdens for banks.

Understanding AI in the Banking Sector

AI in banking refers to using intelligent technologies like machine learning, natural language processing, and advanced analytics to perform tasks that once required human judgment. These systems can analyze data, automate processes, detect patterns, and even “learn” from experience to improve performance over time. Whether it’s catching fraudulent activity in real-time or offering customers a personalized savings plan, AI is adding intelligence to everyday banking operations. It enhances decision-making by providing insights drawn from massive volumes of structured and unstructured data. AI also improves customer service by enabling 24/7 support through virtual assistants and chatbots. Credit scoring and loan approvals are becoming more accurate and inclusive with AI-driven risk models. Additionally, AI helps banks reduce operational costs and improve regulatory compliance through smarter automation.

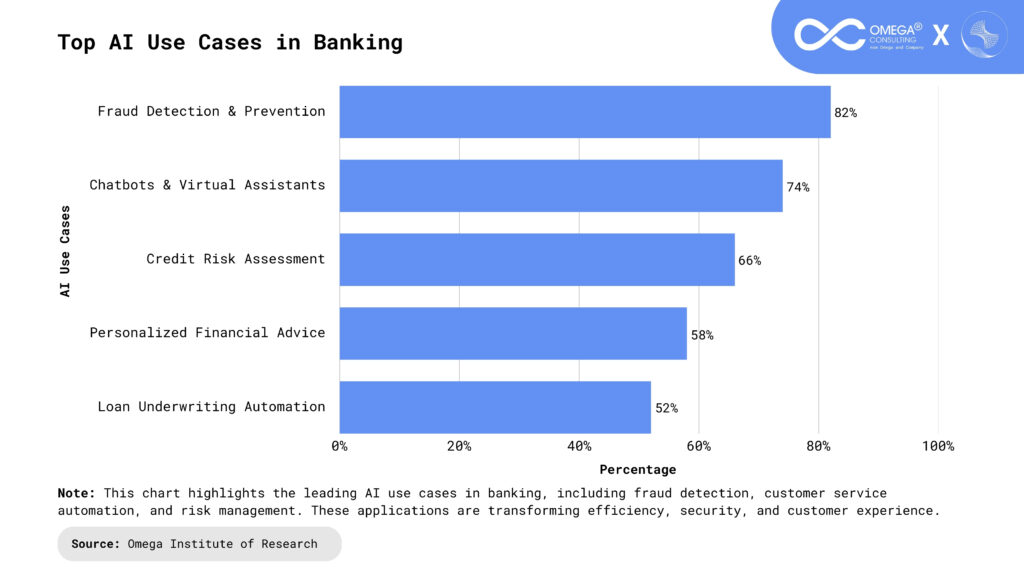

Core Areas Where AI Is Making a Difference

Smarter Customer Interactions with Virtual Assistants: AI-powered chatbots and virtual assistants are revolutionizing customer service. They respond to common queries, help with basic transactions, and can even provide financial advice. Unlike traditional call centers, these tools are always available offering round-the-clock support with near-instant responses. They learn from customer interactions to improve over time, delivering more accurate and personalized responses. These assistants can also escalate complex issues to human agents, ensuring a seamless hybrid service experience.

Real-Time Fraud Monitoring and Alerts: Fraud prevention is a constant concern for banks. AI tools monitor millions of transactions simultaneously to spot unusual behavior. They can instantly flag and block suspicious activity like a sudden large withdrawal from a foreign location protecting both banks and customers. Machine learning models are continuously updated to adapt to emerging fraud patterns. This proactive approach significantly reduces false positives while increasing detection accuracy.

Smarter Lending and Credit Underwriting: AI is rewriting the rules of credit assessment. Instead of relying solely on traditional credit scores, AI systems consider a broader range of data like transaction patterns, bill payment history, and digital footprints. This approach opens up credit access to previously underserved populations. It reduces biases in decision-making and enables faster loan approvals. Additionally, predictive analytics help lenders forecast repayment behavior with higher precision.

AI-Driven Automation of Internal Processes: Banks are using AI to automate labor-intensive processes like document verification, compliance checks, and onboarding. Combined with Robotic Process Automation (RPA), these tools streamline workflows and reduce operational delays. AI helps reduce human errors and ensures consistency in back-office operations. This efficiency allows staff to focus on higher-value tasks, boosting overall productivity.

Data-Driven Personal Finance Insights: AI enables banks to analyze a customer’s financial history and behavior to offer relevant advice and product recommendations. From budgeting tips to investment insights, AI is helping customers make better financial choices. These tools can also forecast future spending trends, helping customers avoid debt and save more effectively. The hyper-personalization fosters deeper engagement and customer loyalty.

AI-Powered Risk and Compliance Tools: AI helps banks stay compliant by constantly scanning changes in regulations and analyzing internal processes for red flags. It also plays a critical role in identifying credit and market risk by analyzing economic trends, customer behavior, and portfolio performance. Natural language processing (NLP) allows AI to interpret regulatory texts faster than human analysts. Furthermore, AI models simulate various risk scenarios to prepare institutions for potential financial shocks.

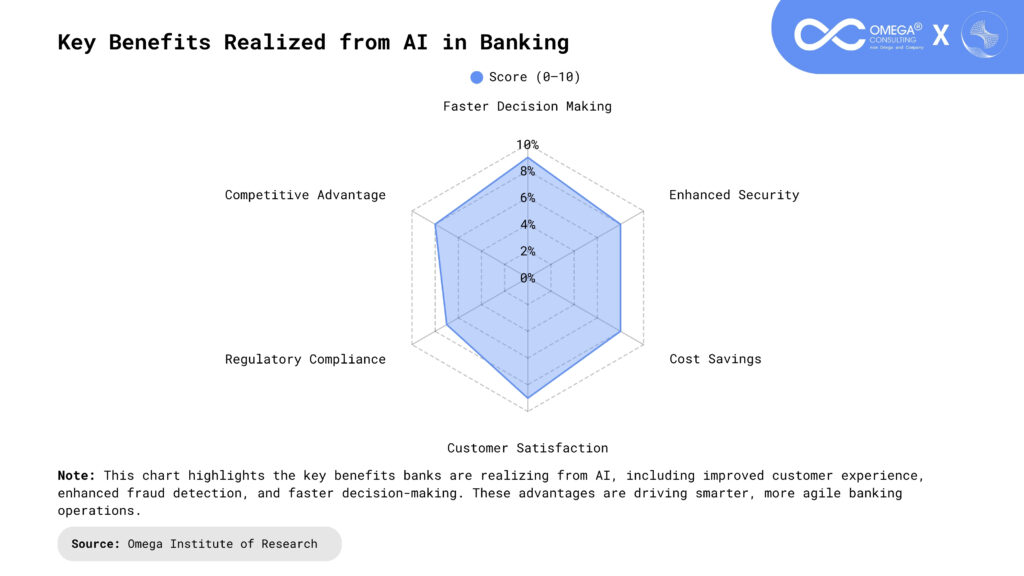

Benefits of AI in Modern Banking

24/7 Availability: One of the most visible benefits of AI in banking is its ability to offer continuous customer support. AI-powered chatbots and virtual assistants are not limited by business hours; they operate around the clock, handling routine queries such as balance inquiries, transaction details, password resets, and even simple loan application steps. This uninterrupted service improves customer satisfaction by reducing wait times and providing immediate solutions, particularly during off-hours, weekends, or holidays when human agents may be unavailable. It ensures that customers always feel supported, no matter when they reach out.

Improved Accuracy: In the highly regulated and detail-oriented world of banking, even small errors can lead to significant consequences. AI reduces the risk of manual mistakes by automating tasks such as data entry, transaction matching, and document processing. Machine learning algorithms continuously learn from data to refine their accuracy over time. Whether it’s verifying a customer’s identity or processing loan applications, AI ensures consistency, precision, and compliance with regulations. This improvement in accuracy not only boosts internal efficiency but also protects institutions from regulatory penalties and reputational damage.

Enhanced Security: Security is paramount in banking, and AI significantly strengthens it. Unlike traditional systems that rely on pre-defined rules, AI uses behavioral analytics to detect unusual patterns in real-time. For example, if a user suddenly logs in from an unfamiliar location or makes a large transaction outside their normal spending habits, the AI can instantly flag or block the activity. Deep learning models are capable of identifying sophisticated fraud schemes and adapting to new tactics as they emerge. This proactive defense mechanism not only protects banks from financial loss but also reassures customers that their money and data are safe.

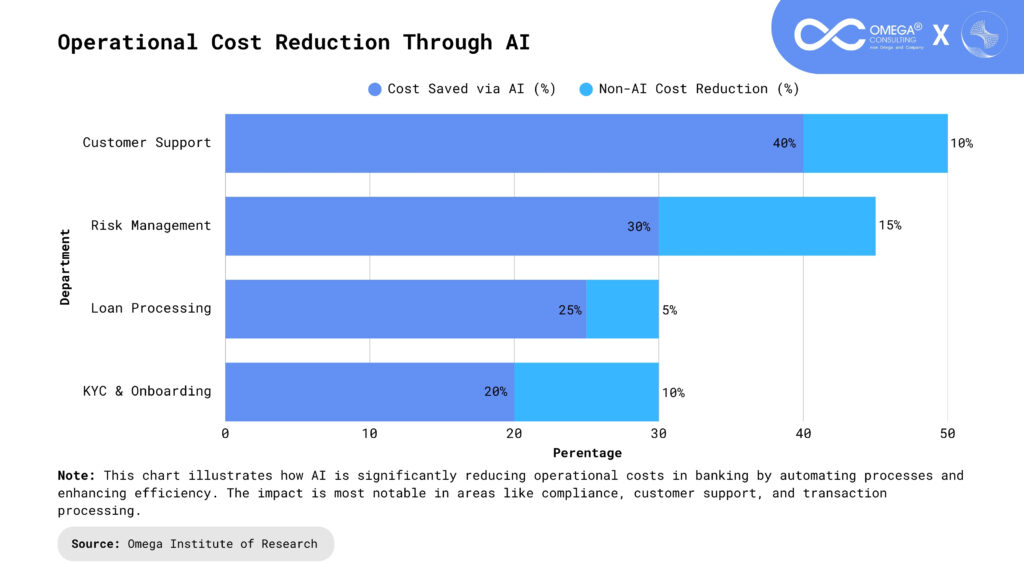

Cost Savings: By automating repetitive and time-consuming tasks such as onboarding, compliance checks, KYC (Know Your Customer) processes, and customer queries banks can significantly reduce their operational overhead. Fewer resources are required to handle high-volume tasks, which leads to more efficient staffing and lower labor costs. Moreover, AI-driven tools can scale easily without proportional increases in cost, making them ideal for institutions aiming to grow without adding administrative burden. These cost efficiencies can then be passed on to customers in the form of better rates or services, creating a competitive edge.

Better Customer Engagement: AI enables banks to offer personalized financial products and services by analyzing a customer’s transaction history, preferences, goals, and even browsing behavior. For example, based on a user’s spending habits, an AI system can suggest customized savings plans, credit card offers, or mortgage options. This level of personalization makes customers feel understood and valued. Additionally, predictive analytics can anticipate customer needs such as suggesting loan pre-approval when rent payments increase thereby improving engagement and deepening the relationship. As a result, customers are more likely to stay loyal to a bank that proactively supports their financial journey.

Challenges to AI Implementation in Banking

Despite its advantages, adopting AI isn’t without obstacles:

Data Privacy & Ethics: AI thrives on data but in banking, that data is highly sensitive. Customer information like income, spending habits, personal identification, and financial history must be handled with extreme care. Improper use or exposure of this data can lead to serious breaches of privacy, legal action, and a loss of customer trust. Moreover, ethical concerns arise when AI algorithms make decisions such as approving or rejecting loans without clear human oversight or explanation. Banks must balance AI innovation with transparency and ensure that their models do not reinforce bias or discrimination. Robust data governance policies, clear consent mechanisms, and explainable AI models are crucial to address these concerns.

Regulatory Complexity: The financial sector is one of the most heavily regulated industries in the world. AI systems in banking must comply with a complex web of local and international regulations concerning data usage, customer rights, risk management, anti-money laundering (AML), and fair lending practices. Regulators now require institutions to explain how AI models make decisions, a concept known as “model interpretability” or “explainability.” Ensuring AI systems remain compliant as laws evolve adds another layer of complexity. Non-compliance can result in hefty fines, reputational damage, and a loss of operating licenses. Therefore, regulatory risk is a major hurdle to widespread AI adoption.

Technology Gaps: Many banks still rely on decades-old legacy systems that are not designed to handle modern AI workloads. These systems often operate in silos, lack integration capabilities, and are limited in terms of processing speed and data availability. Integrating AI tools into such outdated infrastructure can be both technically challenging and costly. In some cases, institutions may need to completely overhaul their IT architecture, migrating to cloud-based platforms, modernizing databases, and building APIs for real-time data access. Without these foundational changes, the full potential of AI cannot be realized, and performance may be inconsistent or unreliable.

Human Capital: Even with the right tools and infrastructure, AI success depends heavily on talent. There’s a growing global shortage of skilled professionals in AI, machine learning, data engineering, and cybersecurity. Banks need experts who can design, train, deploy, and maintain AI models while also understanding the unique regulatory and operational nuances of the financial sector. Additionally, non-technical staff need training to work alongside AI systems, interpret results, and make informed decisions. Building cross-functional teams that include data scientists, compliance officers, and domain experts is critical but recruiting and retaining this talent is a major ongoing challenge.

What the Future Holds: AI Trends in Banking

AI’s role in banking will only deepen in the coming years. Some emerging trends to watch:

Voice Banking: Voice-enabled AI is poised to redefine how users interact with financial institutions. Imagine asking your bank account, through your smart speaker or mobile device, “What’s my current balance?” or “Did my paycheck arrive?” and getting an instant response hands-free. As natural language processing (NLP) and speech recognition improve, voice banking will become more secure and context-aware. Customers will be able to initiate transfers, pay bills, and even receive spending insights through simple voice commands. This will not only boost accessibility for visually impaired users or those less tech-savvy, but also create more intuitive and frictionless banking experiences.

Emotion AI: Emotion AI, also known as affective computing, is an emerging area where AI can detect and interpret human emotions through voice tone, facial expressions, text sentiment, or behavioral patterns. In banking, this can transform customer service interactions. For example, if a chatbot detects frustration in a customer’s voice or language, it can escalate the issue to a human agent or adapt its tone to show empathy. Emotion-aware systems could also help identify at-risk customers for instance, someone feeling overwhelmed about debt and proactively offer support or financial counseling. This emotional intelligence enhances user trust, satisfaction, and long-term loyalty.

AI + Blockchain: The integration of AI and blockchain technology has the potential to revolutionize how financial data is processed, stored, and secured. While blockchain offers transparency, immutability, and decentralization, AI brings intelligent automation and data analysis capabilities. Together, they can improve everything from fraud detection to identity verification and smart contract execution. For example, AI can monitor blockchain transactions in real time to detect anomalies or predict market trends, while blockchain ensures that the data feeding those AI models is tamper-proof. This synergy can enable more trustworthy, efficient, and decentralized banking ecosystems particularly in cross-border payments, lending, and compliance.

Embedded AI in Mobile Apps: Mobile banking apps are evolving into intelligent financial advisors, thanks to embedded AI. These in-app assistants analyze user behavior, transaction history, and financial goals to provide personalized insights like flagging overspending, suggesting budget adjustments, or recommending investment opportunities. Instead of simply checking balances or transferring funds, users will interact with their bank apps for daily financial guidance, predictive alerts, and goal tracking. This shift will make banking apps not just tools for transactions, but proactive partners in financial well-being. With AI embedded natively, these apps can continuously learn and adapt to the user’s life stage, habits, and preferences.

Conclusion

AI is turning banking into a faster, smarter, and more personalized experience. It’s not just about technology, it’s about creating meaningful value for both customers and institutions. From better service to smarter decisions and stronger security, AI is helping banks adapt to a digital economy and meet the rising expectations of tech-savvy consumers. It enables banks to deliver hyper-personalized financial guidance, streamline internal operations, and respond proactively to market shifts and customer needs. As AI continues to evolve, it will become even more embedded in every layer of banking, from risk assessment to customer engagement. For banks looking to lead rather than follow, now is the time to invest in AI not just as a tool, but as a core part of their strategy, culture, and long-term vision.

- https://cloud.google.com/discover/ai-in-banking

- https://www.ibm.com/think/topics/ai-in-banking

- https://www.techtarget.com/searchenterpriseai/feature/AI-in-banking-industry-brings-operational-improvements

- https://www.db.com/what-next/digital-disruption/better-than-humans/how-artificial-intelligence-is-changing-banking/index?language_id=1

- https://www.vonage.com/resources/articles/ai-in-banking/

Subscribe

Select topics and stay current with our latest insights

- Functions