- Industries

Industries

- Functions

Functions

- Insights

Insights

- Careers

Careers

- About Us

Economic Uncertainty and Rising Costs

Amid a rapidly shifting global economy, economic uncertainty and rising costs have become pressing challenges for both consumers and businesses. Inflation continues to climb, and achieving financial stability is becoming increasingly difficult, forcing individuals and organizations to reevaluate how they allocate and manage resources. Geopolitical tensions, supply chain disruptions, and evolving consumer behavior are further amplifying financial volatility, putting pressure on household budgets and corporate profitability alike. Small businesses face shrinking margins, while families must make difficult decisions about spending and saving. In response, proactive financial planning, digital innovation, and strategic policy interventions are emerging as essential tools for adaptation. This article explores the root causes, widespread impacts, and actionable solutions to navigate and overcome these challenging economic times.

Understanding Economic Uncertainty

Economic uncertainty means unpredictable changes in financial and market conditions, making it hard to plan for the future. This slows down decision-making, reduces investments, and increases overall market anxiety. The main contributors to this uncertainty include:

Government policies and regulations: Unforeseen tax changes, tariff implementations, or regulatory reforms create instability. These shifts can disrupt corporate planning and hinder long-term investment decisions. International policy differences can further complicate global trade. Changes in leadership or elections can alter business-friendly environments. This leads to hesitancy in cross-border collaboration and risk-taking.

Market volatility and interest rates: Constant changes in stock prices, commodity rates, and borrowing costs make it difficult to plan budgets. Investors often withdraw capital or move to safer options during market swings. High interest rates reduce consumer borrowing, affecting housing and auto markets. Low rates may lead to bubbles in risky assets. Uncertainty discourages innovation and long-term commitments.

Global crises and unexpected events: Disasters like pandemics, wars, or cyberattacks cause economic slowdowns and disrupt supply chains. These events can result in unemployment, increased national debt, and global inflation. Recovery requires coordinated international efforts and strong fiscal policy. Global confidence drops when multiple regions are affected simultaneously. Business continuity becomes a major concern for companies operating across borders.

What’s Driving Rising Costs?

Rising costs or inflation occurs when prices for goods and services increase over time, reducing purchasing power. Inflation is a result of several overlapping economic pressures. Key drivers include:

Supply chain issues and shipping delays: Global logistics problems make transporting goods slower and more expensive. Shortages of key components like semiconductors have halted production in many industries. Shipping containers and fuel costs have surged, raising prices for nearly every product. Inventory gaps force companies to pay premiums for expedited services. Customer dissatisfaction also grows due to unpredictable delivery times.

Energy and fuel price surges: Unpredictable changes in oil and gas prices affect manufacturing, transportation, and power generation. As energy becomes more expensive, operating costs rise across sectors. Households face higher utility bills, straining budgets. Geopolitical conflicts and environmental policies can both cause fuel price shocks. Companies that rely on logistics and machinery face compounding expenses.

Labor shortages and wage hikes: As businesses compete for talent, wages are increasing across many industries. Rising payroll costs are being passed on to consumers through higher product prices. Remote work trends and skill mismatches add complexity. Industries like healthcare, logistics, and food services are hardest hit. High employee turnover and recruitment challenges impact long-term planning.

Impact on Households

Families and individuals are directly affected by the changing economic environment. The rising cost of living means reevaluating spending priorities and saving strategies. Major impacts include:

Higher living expenses: The price of essentials like groceries, fuel, electricity, and rent has surged. Disposable income shrinks, limiting options for recreation, travel, or dining. Families may need to dip into savings to cover regular expenses. Inflation disproportionately impacts low- and middle-income households. Many are also turning to debt or credit to make ends meet.

Reduced ability to save or invest: With rising costs, fewer households can set money aside for emergencies or retirement. Investments may yield less as inflation eats into returns. Financial goals like buying a home or funding education are delayed. Fear of market volatility makes people risk-averse. The long-term impact is weakened financial security.

Increased stress and lifestyle changes: People are forced to cut back on non-essential expenses like entertainment or personal care. Rising financial pressure contributes to anxiety and relationship strain. Families may move to lower-cost areas or take second jobs. Mental well-being is deeply affected by constant economic pressure. Health-related expenses may be postponed, leading to long-term consequences.

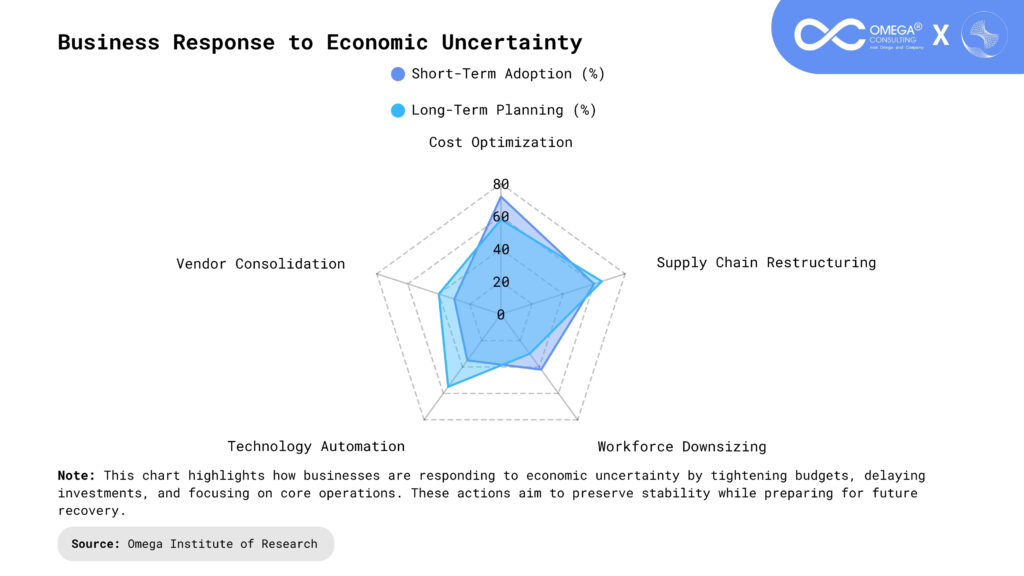

Impact on Businesses

Businesses are experiencing severe operational challenges due to both rising costs and economic instability. This forces them to make tough decisions about pricing, staffing, and expansion. Key impacts include:

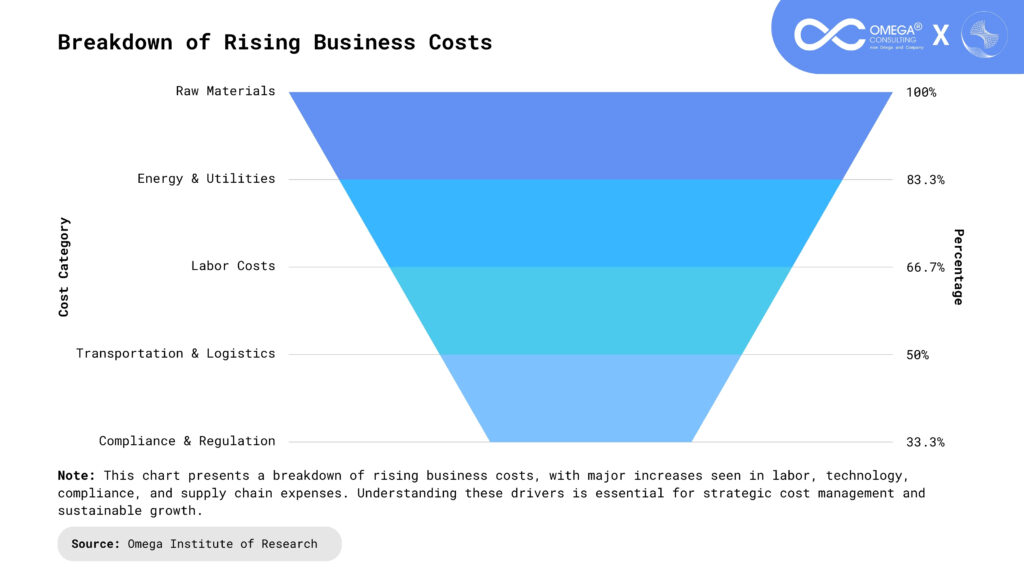

Shrinking profit margins: Raw materials, transportation, and wages are all more expensive, eroding profits. Companies may need to raise prices, risking customer loyalty. Budget cuts often affect marketing, training, and innovation. Many businesses operate at break-even levels. Access to affordable credit is also reduced in high-rate environments.

Shifting customer behaviors: Consumers are delaying non-essential purchases and switching to more affordable brands. This affects revenue and changes demand patterns. Loyalty becomes harder to maintain without offering added value. Companies must gather real-time customer insights. Flexibility in product offerings becomes essential to survival.

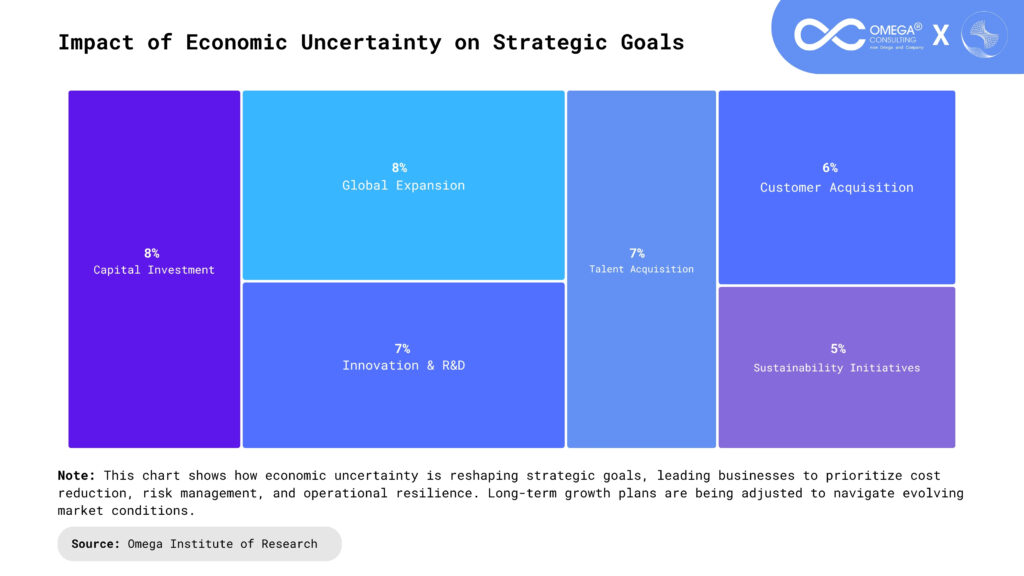

Operational and strategic reevaluation: Businesses are rethinking everything from supply chain management to staffing models. Many are investing in automation to reduce labor dependency. Geographic diversification is being considered to lower regional risks. Decision-makers are prioritizing cost-efficiency over growth. Mergers and acquisitions may increase as companies seek scale.

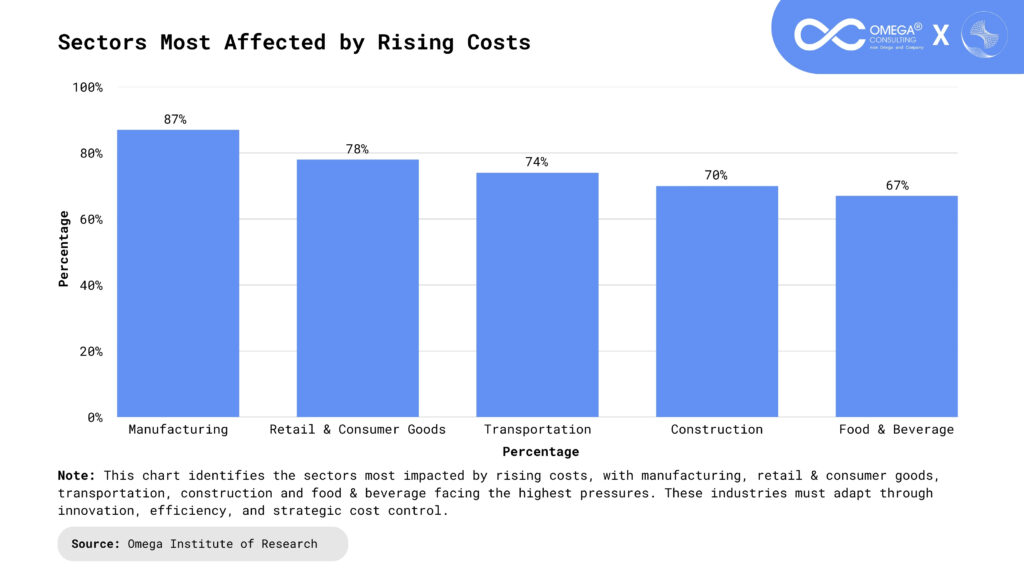

Sectors Most Affected

While all sectors feel the effects of rising costs, some are disproportionately impacted. These industries face compounding issues that make recovery slower and harder. Key vulnerable sectors include:

Retail and e-commerce: Rising logistics and product costs affect margins, while customers shop more cautiously. Inventory misalignment and demand fluctuations hurt profitability. Discount-driven competition erodes pricing power. Smaller players struggle to compete with large-scale marketplaces. Retailers are rethinking loyalty and personalization strategies.

Manufacturing and construction: Both rely heavily on energy, transportation, and skilled labor. Delays in raw materials and compliance costs drive up project budgets. Workforce shortages extend timelines and increase errors. Infrastructure costs are difficult to predict or control. Clients may cancel or postpone projects due to budget uncertainty.

Travel, tourism, and hospitality: These industries are highly sensitive to inflation, global unrest, and public health issues. Fuel costs and staffing gaps reduce margins, while customer demand remains inconsistent. International travel is affected by visa delays and currency volatility. Service quality suffers due to understaffing. Smaller operators are especially vulnerable to economic shocks.

How Can Individuals Cope?

Though the financial climate is challenging, individuals can still take proactive steps to build security. By adopting disciplined financial practices, people can increase resilience. Long-term planning is more important than ever. Here’s how to cope:

Create and follow a detailed budget: Outline income, fixed costs, and discretionary expenses to find savings opportunities. Use tools or apps to monitor spending patterns. Prioritize essential needs and minimize impulse purchases. Budgeting empowers better financial decisions. It also helps you track progress toward goals.

Build a robust emergency fund: A dedicated savings account can cover 3–6 months of living expenses. It helps avoid taking on debt during unexpected job loss or emergencies. Start small with consistent contributions. Keep the fund liquid and accessible. Emergency funds provide peace of mind in uncertain times.

Invest with long-term goals in mind: Diversify investments to spread risk across different asset classes. Consider inflation-protected instruments and index funds. Rebalance portfolios regularly based on changing conditions. Avoid panic during short-term market drops. A long view helps weather economic storms.

How Can Businesses Adapt?

Companies that act strategically and adapt quickly can survive and even grow during uncertainty. Resilience, innovation, and agility are key traits. Practical solutions include:

Implement cost-control initiatives: Review every operational cost and eliminate inefficiencies. Invest in automation and digitization to streamline workflows. Conduct supplier renegotiations or find cost-effective alternatives. Lean operations improve margins and reduce risk. Empower teams to identify internal savings.

Explore alternative supply chains: Diversify sourcing strategies and avoid dependency on single regions. Build relationships with multiple vendors for flexibility. Consider reshoring or nearshoring options. Improve inventory forecasting through real-time data. Supply chain agility reduces downtime and volatility.

Enhance customer relationships: Offer personalized service, loyalty rewards, and transparency to build trust. Use feedback to adapt products and messaging. Communicate openly about necessary price changes. Value-driven experiences help maintain the customer base. Empathy and responsiveness win loyalty in tough times.

The Role of Government and Central Banks

Governments and central banks shape economic outcomes through fiscal and monetary policies. Their timely action is vital in managing inflation and uncertainty. Their tools include:

Adjusting interest rates: Central banks raise rates to control inflation or lower them to stimulate growth. This affects everything from mortgages to business loans. Interest rates directly influence consumer and business behavior. Missteps can lead to recessions or asset bubbles. Transparent communication from central banks builds market confidence.

Providing stimulus and support: Emergency funding, tax relief, and subsidies help individuals and businesses survive downturns. Targeted support ensures equitable recovery across sectors. Governments must act swiftly and efficiently. Long-term infrastructure investments can boost employment. Social safety nets must be updated for modern challenges.

Regulatory oversight and reforms: Updating outdated laws, simplifying compliance, and ensuring fair competition are crucial. Government stability encourages investor confidence. Clear rules help small businesses compete fairly. Reforms should encourage innovation and job creation. Oversight prevents monopolies and financial abuse.

Looking Ahead: A Future with Caution and Opportunity

Though the road ahead is uncertain, history proves that crises often create room for innovation and reform. A flexible mindset and readiness to evolve are essential. Here’s what lies ahead:

Innovation thrives under pressure: Challenging times force companies and individuals to think creatively. New technologies and services are often born during downturns. Entrepreneurship grows as traditional paths shrink. Constraints drive smarter solutions. Economic pain can fuel meaningful progress.

Digital transformation accelerates: Businesses are rapidly digitizing operations to reduce costs and improve service. AI, automation, and cloud computing drive efficiency. Remote work and virtual services are becoming permanent. Digitization helps businesses stay agile. It also opens new global opportunities.

Stronger financial awareness: Economic hardship encourages people to become financially literate. Budgeting, investing, and debt management are gaining attention. Schools and workplaces are offering financial education. Informed citizens make smarter choices. Financial wellness becomes a cultural priority.

Conclusion

Economic uncertainty and rising costs are changing the way we think, spend, and plan. But within these challenges lie opportunities to innovate, rebuild, and prepare for a more resilient future. By understanding the forces at play and responding wisely, individuals and businesses can not only survive but grow stronger through adversity. Embracing agility, leveraging technology, and fostering collaboration will be critical in adapting to this evolving economic landscape. Strategic investments in sustainability, efficiency, and upskilling can turn short-term obstacles into long-term gains. Ultimately, resilience isn’t just about weathering the storm—it’s about emerging better equipped for the road ahead.

- https://www.sciencedirect.com/science/article/abs/pii/S1572308920301443

- https://www.nature.com/articles/d41586-025-02200-x

- https://www.mdpi.com/2227-9091/11/4/66

- https://pmc.ncbi.nlm.nih.gov/articles/PMC8563472/

- https://www.economicsobservatory.com/why-uncertainty-so-damaging-economy

Subscribe

Select topics and stay current with our latest insights

- Functions